FORD PRO

Ford Pro only captured value at the point of vehicle sale to dealers. Everything downstream — finding an upfitter, sourcing parts, coordinating installation, arranging delivery — happened in a fragmented ecosystem running on phone calls, paper catalogues, and personal referrals. The upfitting industry, worth an estimated $9–12B in North America, was operating with almost no technological sophistication. Ford Pro’s CTO wanted the full picture: behaviours, relationships, pain points, and hidden dynamics across the commercial upfitting value web, with the goal of finding strategic openings to move downstream and build something defensible.

What I did

I co-led a 4-person Humanistic team through an 8-week engagement structured around two parallel workstreams: ethnographic research with industry insiders and a comprehensive market and competitive landscape analysis.

We operated at arm’s length from Ford, positioning ourselves as a third-party research firm rather than an OEM proxy. The upfitting industry runs on personal relationships and deep skepticism toward manufacturers getting involved in their business. That positioning got upfitters, parts distributors, and independent dealers to open up about competitive dynamics, pricing structures, and technology hesitations they would have guarded in a direct OEM conversation.

We conducted in-depth interviews across five upfitting shops, speaking with 15–20 individuals in roles spanning shop ownership, installation, sales, and parts procurement, plus dealers and commercial fleet customers. The conversations surfaced entrenched orthodoxy (paper catalogues persisting because digital alternatives required structured data no one had incentive to organize), process opacity between all parties, and real fear about disruptive technologies eliminating the relationships that kept the industry functioning.

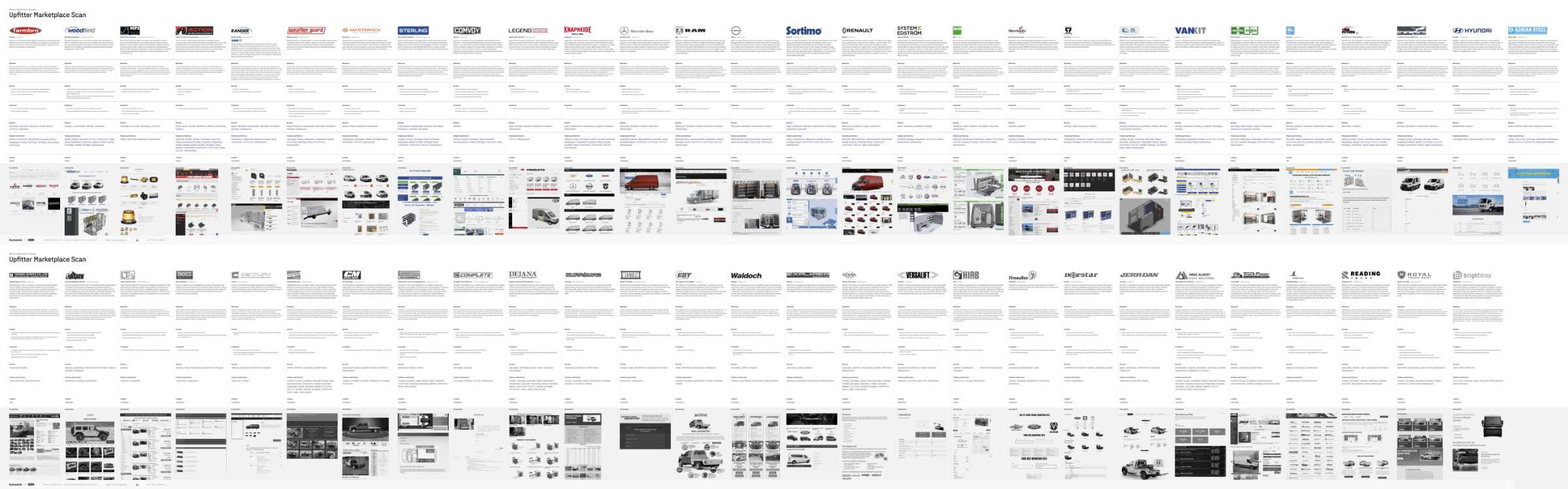

The output of the competitive marketplace scan

I chose to map the ecosystem as an actor-based value web rather than a linear journey. The value web showed the flow of value, information, and dependency between six actor types (OEMs, dealers, upfitters, parts manufacturers, used vehicle sellers, and services vendors), exposing where Ford sat in the system (upstream, one-directional) and where it could insert itself to create reciprocal value downstream. In parallel, I led a competitive scan profiling dozens of players — Ranger Design, Work Truck Solutions, Knapheide, Adrian Steel, and others — evaluating each across business viability, technology sophistication, UX, risk, and customer value.

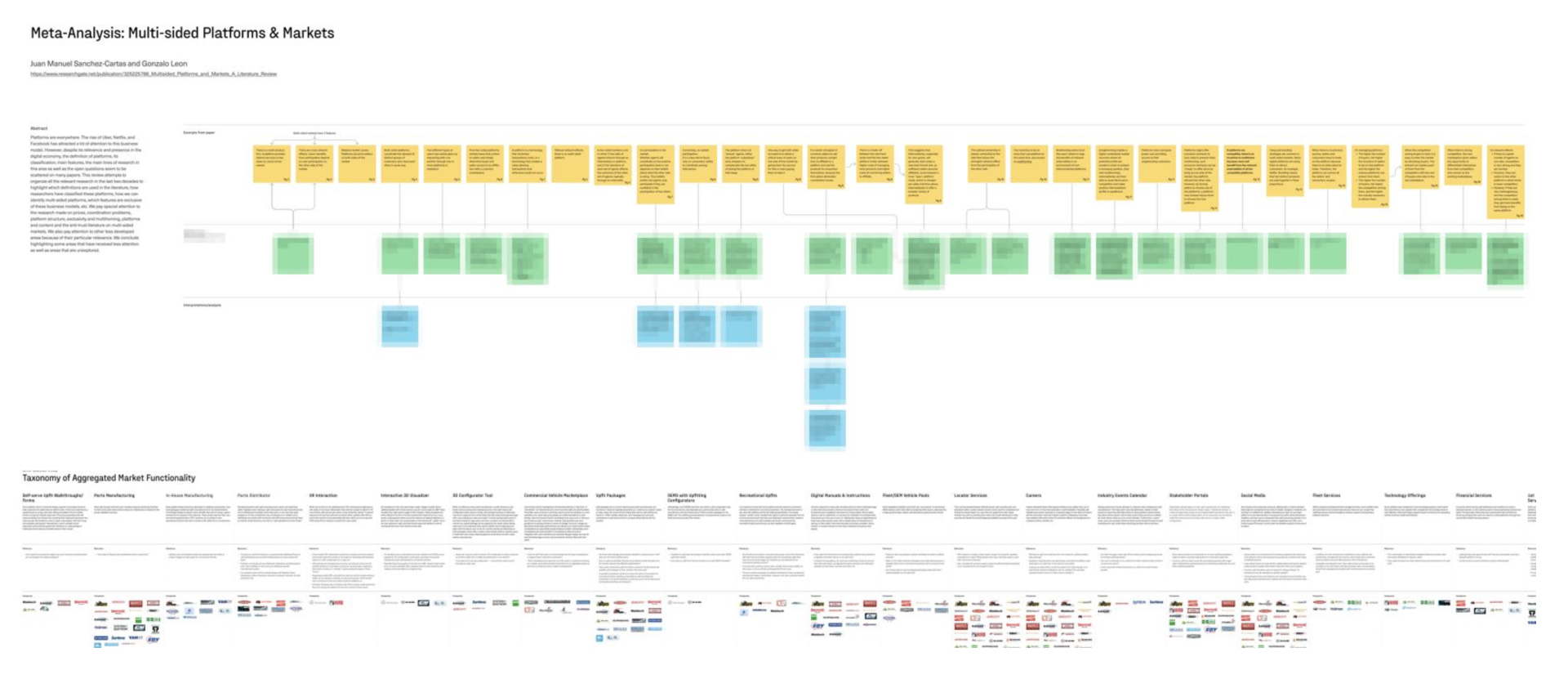

A multi-sided marketplace meta-analysis to determine functionality coverage

From this research I synthesized five opportunity areas mapped to the customer journey: upfit research and consultation tools, a commercial vehicle marketplace, an upfitter vendor marketplace, a parts marketplace replacing paper catalogues, and a value-add services marketplace for branding, delivery, and fleet management. For each, I developed structured build-vs-buy-vs-partner recommendations with competitive benchmarking, risk assessment, and technology evaluation.

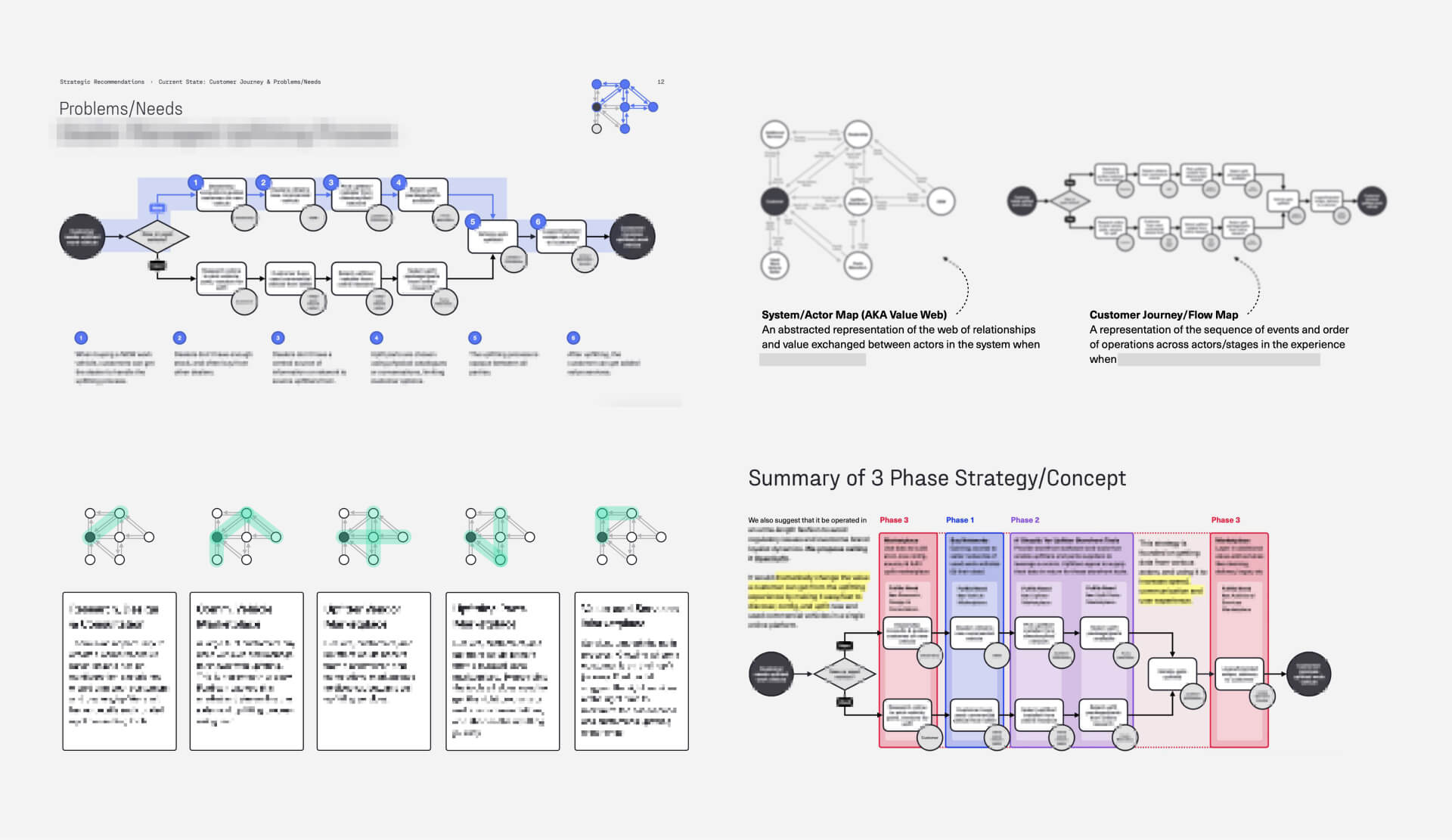

The strategic synthesis was a three-phase marketplace roadmap designed to compound through data accumulation:

Phase 1 — Partner with existing vehicle seller networks (specifically Work Truck Solutions) for immediate inventory data access.

Phase 2 — Build “Shopify-style” storefront tools for upfitters, trading e-commerce capability for structured product data.

Phase 3 — Use accumulated data to launch a massive online upfitting platform consolidating vehicle search, parts sourcing, configuration, financing, and services.

A excerpt from the strategy showing diagrams and marketplace dynamics

One critical framing decision: I argued the marketplace should be OEM-agnostic, operated at arm’s length under a separate brand. Small fleet owners buy used vehicles from whatever manufacturer has available inventory — a Ford-only marketplace would exclude the majority of the addressable market. Ford’s advantage would come from controlling the infrastructure and data layer, not from restricting participation.

Outcomes

$9–12B addressable market identified and mapped

Ford Pro got a quantified picture of the downstream value they were leaving on the table by only capturing revenue at vehicle sale.

5 opportunity areas with build/buy/partner recommendations delivered

The three-phase strategy provided a sequenced roadmap balancing speed-to-market through partnerships with long-term platform ownership through building. Six deliverable modules served as the foundation for subsequent internal strategy work.

One of 6 modules shipped as strategy

The strategy is now in production

In March 2025, Ford Pro launched LocateFordWorkTrucks.com in direct partnership with Work Truck Solutions — the specific Phase 1 partnership we recommended in 2022. The tool enables customers to search for and locate work-ready trucks and vans from Ford dealer inventory nationwide, embedded directly into FordPro.com. By May 2026, Ford Pro began requiring all Commercial Vehicle Center dealers to maintain an active Work Truck Solutions subscription, making what we recommended as a strategic partnership into mandatory dealer infrastructure.

What I learned

Operating at arm’s length from the client during research wasn’t just a tactic for candid interviews. It surfaced an entire category of insight about industry power dynamics and technology resistance that would have been invisible in a direct OEM engagement. That framing decision shaped every recommendation, including the arm’s-length marketplace brand proposal, which echoed the same principle at a strategic level.